The 98th Academy Awards recently awarded Best Picture to “One Battle After Another,” which we feel is a fitting metaphor for the market’s current mood.

Much like Leonardo DiCaprio’s Bob Ferguson, investors have endured a steady barrage of challenges: geopolitical shocks, fiscal uncertainty, trade tensions, technological disruption, and episodic market selloffs – all the while this multi-year bull market struggles to press forward.

Below we break down each of the principal risks shaping the current landscape:

The Iran War

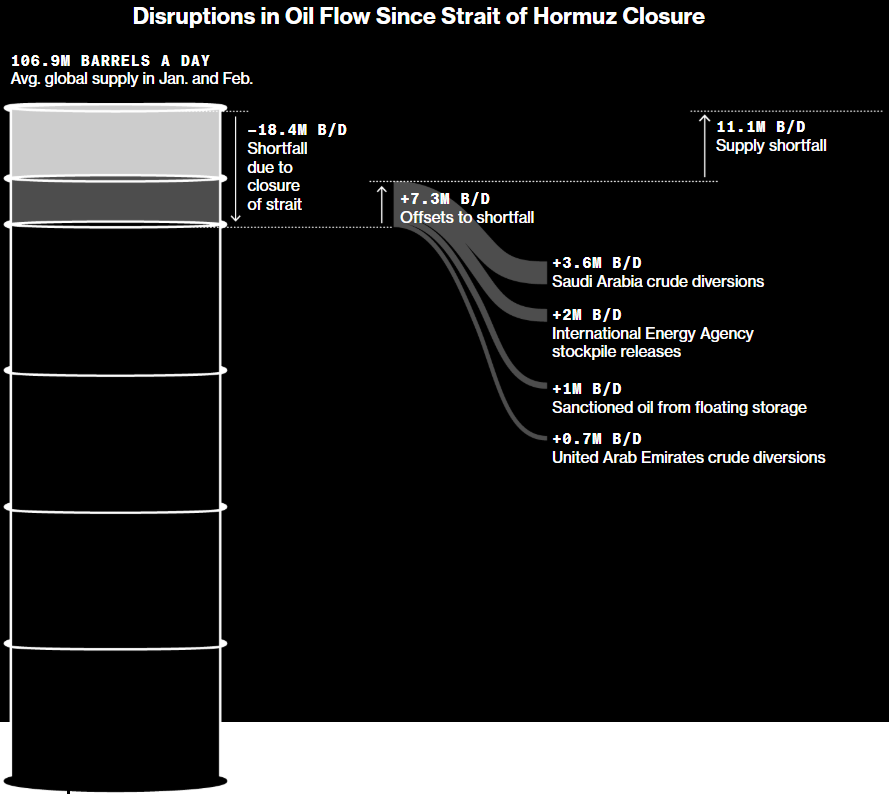

The now month-long conflict involving the U.S., Israel, and Iran has led to the effective closure of the Strait of Hormuz—disrupting the flow of roughly 20 million barrels of oil and refined products per day.

Source: Bloomberg News, “The Strait of Hormuz Oil Shock Is Now Heading West”, Bloomberg L.P., 3/29/26

Iran’s primary leverage lies in its continued threat to target oil tankers transiting the strait, driving energy prices higher. However, the implications extend well beyond oil and gas. The disruption also constrains the global supply of fertilizers (urea, potash, ammonia), petrochemicals (methanol, ethylene), and helium. Given that approximately one-third of global fertilizer and helium flows pass through this chokepoint, the downstream effects could impact food production, semiconductor manufacturing, and medical equipment.

Source: BCA Research – BCA’s Iran Conflict Daily Dashboard, 4/8/2026

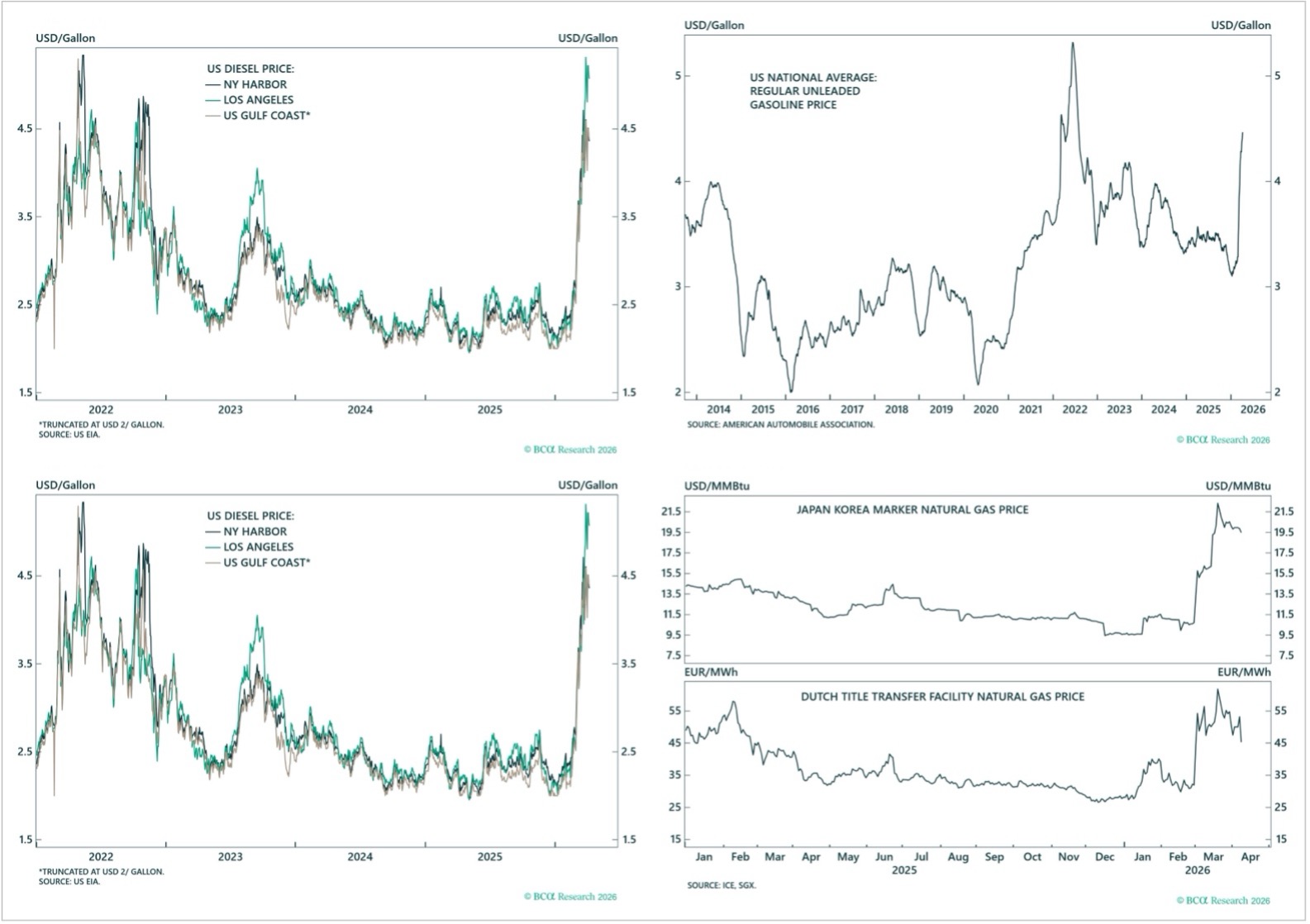

While comparisons to the inflationary oil shocks of the 1970s are understandable, today’s energy market is far more diversified. U.S. shale production, strategic petroleum reserves, and alternative energy sources help mitigate the impact of supply disruptions. A more relevant comparison may be the early 1990s Gulf War. During that period, rising oil prices initially lifted inflation expectations and delayed Federal Reserve easing, while higher input costs weighed on consumption and corporate margins. These pressures ultimately pushed the economy into recession, prompting the Fed to cut rates aggressively—and contributing to George Bush’s loss in the 1992 election.

Recent experience also recalls the 2022 energy price shock, when Russia’s invasion of Ukraine intensified already elevated inflation pressures. Today, the setup differs in important ways. Softer labor market conditions mean that a prolonged energy shock could weigh more heavily on economic growth, reducing both consumer purchasing power and industrial output. While a full-blown U.S. recession may not be in the cards due to the offsetting tailwinds of artificial intelligence, deregulation and tax cuts, international economies dependent upon energy imports – particularly in Asia where they are already taking emergency energy conservation measures – are bracing for potentially more dire consequences.

The recently agreed two-week ceasefire, which should reopen the Strait of Hormuz, is expected to provide some relief to global energy markets. The sooner a permanent agreement is reached, the more limited the economic fallout will be. However, a persistent risk premium is likely to remain in energy markets, and prices are unlikely to return to pre-war levels for an extended period.

Tariffs

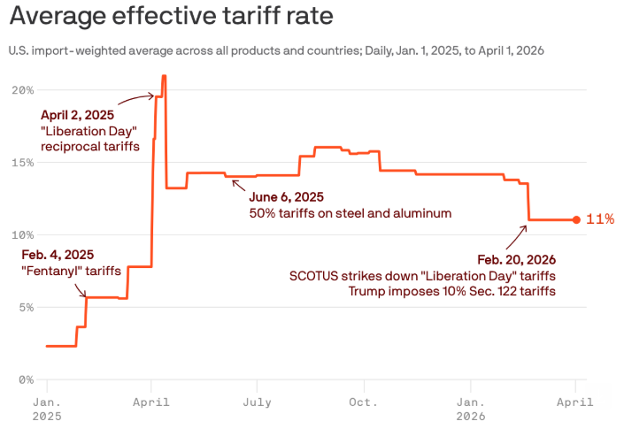

Tariffs continue to function as a tax on economic activity. Despite the Supreme Court’s February ruling limiting the use of the International Emergency Economic Powers Act (IEEPA) for tariff implementation, the administration has pivoted to alternative legal mechanisms, including Section 122 of the Trade Act of 1974, to maintain current tariff levels.

Source: Yale Budget Lab; Chart: Erin Davis/Axios Visuals

While businesses and consumers have thus far absorbed these costs with relative resilience, tariffs continue to work their way through the economy and represent an additional layer of friction in an already fragile macroeconomic environment.

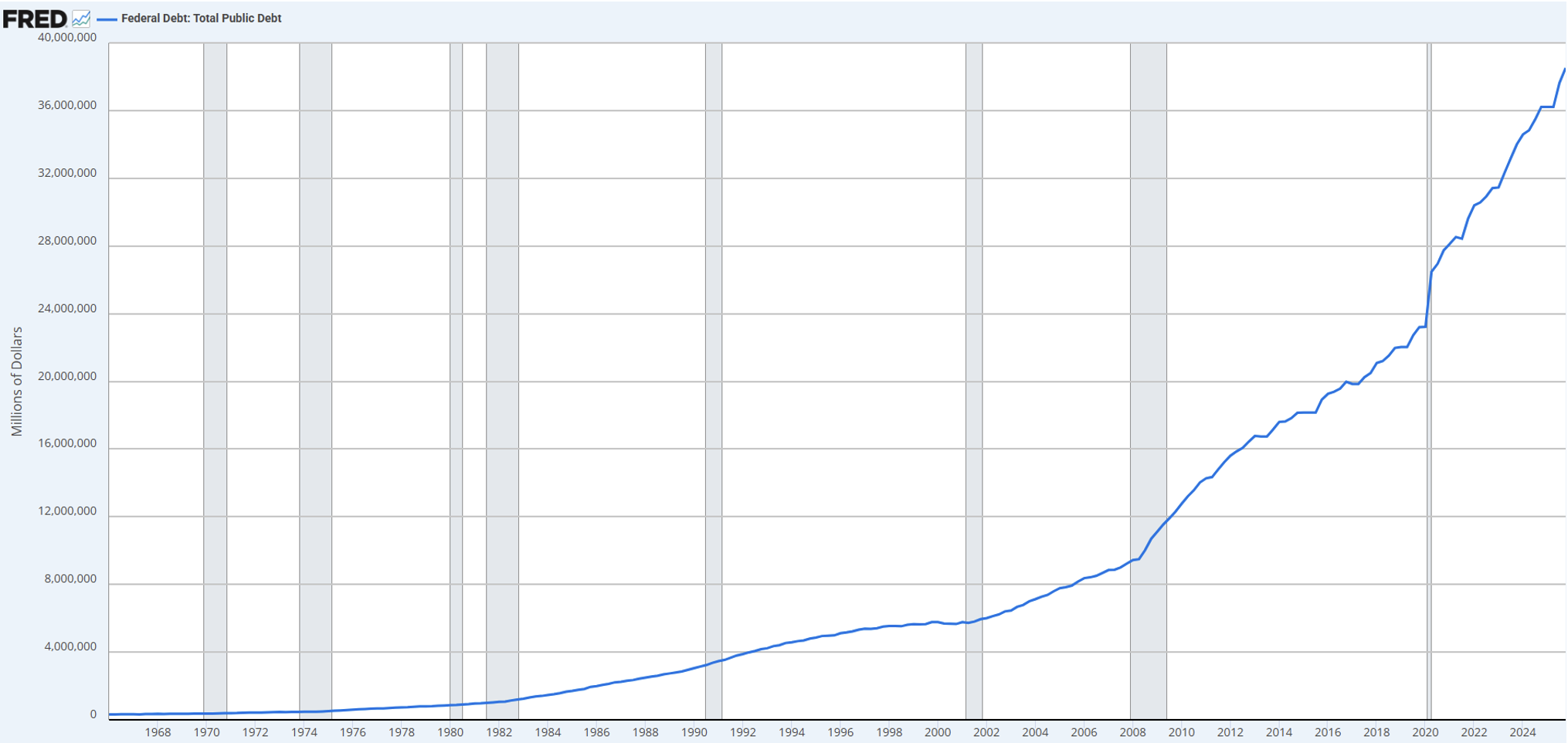

US Federal Budget Deficit

The tariff ruling also introduces fiscal implications, including the potential for up to $165 billion in Treasury refunds—undermining a key component of deficit reduction efforts.

More broadly, the trajectory of U.S. fiscal policy remains a structural concern. Federal debt has risen from approximately $23 trillion pre-pandemic to roughly $38 trillion today—a 65% increase in just six years. Despite periodic calls for fiscal discipline, there has been limited political appetite to meaningfully address the issue.

Source: U.S. Department of the Treasury. Fiscal Service via FRED®

Elevated deficits and rising debt-to-GDP levels increase the long-term risk of U.S. dollar debasement. While not an immediate threat, this dynamic reinforces the importance of maintaining exposure to real and risk assets over time, rather than relying solely on cash holdings vulnerable to erosion in purchasing power.

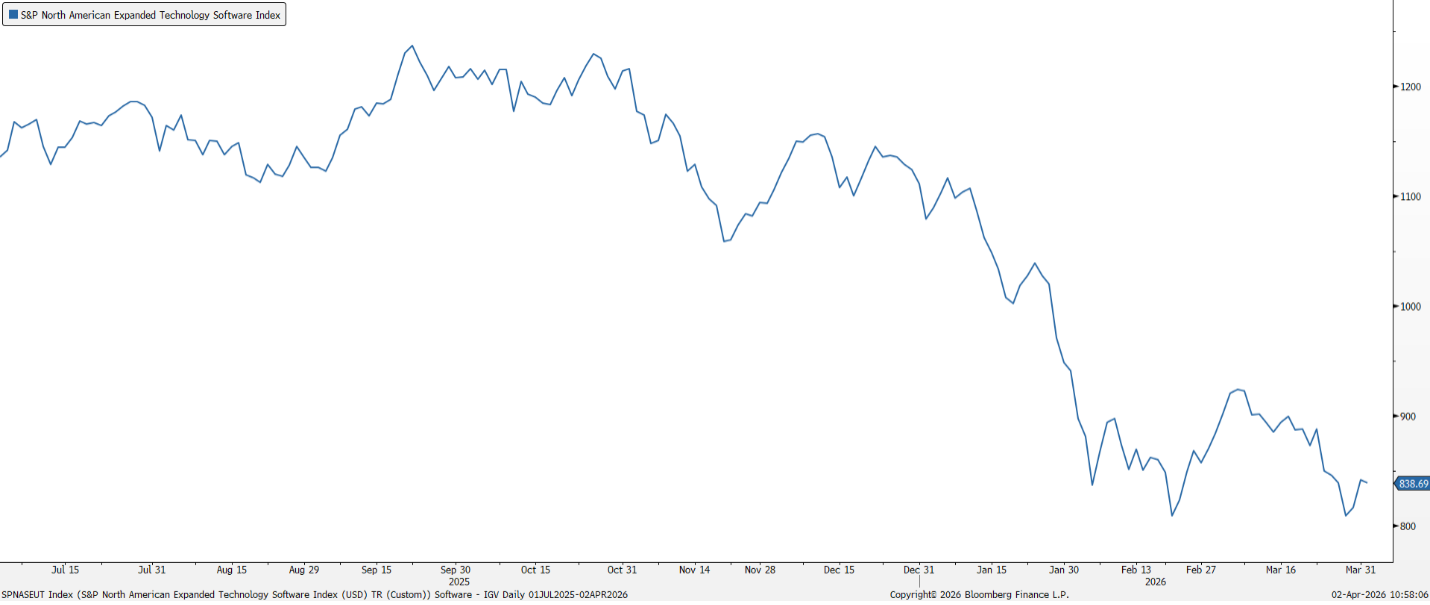

“SaaS-pocalypse”

Software-as-a-service (SaaS) equities have experienced notable multiple compression in recent months, driven by concerns that artificial intelligence may render legacy software models obsolete.

Source: Bloomberg L.P.

We believe the market’s reaction has been overly indiscriminate. There is a meaningful distinction between simple, single-user tools that may be vulnerable to AI displacement and deeply embedded enterprise platforms characterized by high switching costs, proprietary data, and mission-critical functionality.

In many cases, the current environment reflects short-term multiple compression rather than permanent impairment of business value. We have selectively added to software positions where we believe companies are well-positioned not only to withstand AI disruption, but to leverage it as a competitive advantage.

Private Credit

Concerns in public SaaS markets have spilled over into private credit, where software companies represent approximately 20% of borrowers. Recent headlines highlighting liquidity pressures and redemption caps have raised concerns among retail investors, particularly given lingering sensitivities from the Global Financial Crisis.

It is important to distinguish today’s private credit market from the pre-2008 financial system. The modern $3 trillion private credit ecosystem emerged in response to post-crisis banking regulations, which constrained traditional lenders. Private credit structures typically include negotiated covenants, private equity sponsorship, and lower levels of structural leverage than the securitized mortgage products that drove systemic risk in 2008.

Redemption caps in private credit vehicles—typically 5% per period—have been triggered across several funds that have catered to retail investors. These redemption caps are not a sign of market disfunction but rather structural design features intended to align investor liquidity with the underlying illiquid assets – avoiding fire sales and protecting remaining investors during periods of elevated redemption demand.

Should the economy enter a slowdown or recession, default rates will surely rise and private credit (like many other risk assets) will experience more modest returns. There will undoubtedly be some funds that run into trouble due to high levels of leverage, loan concentration and sub-par underwriting.

Remember Warren Buffett’s famous quote:

At this stage, however, the financial health of these borrowers does not support the alarmist headlines and does not pose a systemic risk.

What To Do

Each of these risks warrants monitoring, but few rise to the level of an existential threat for diversified, high-quality portfolios. We recommend maintaining adequate liquidity, prioritizing balance sheet strength, and selectively capitalizing on dislocations as they arise.

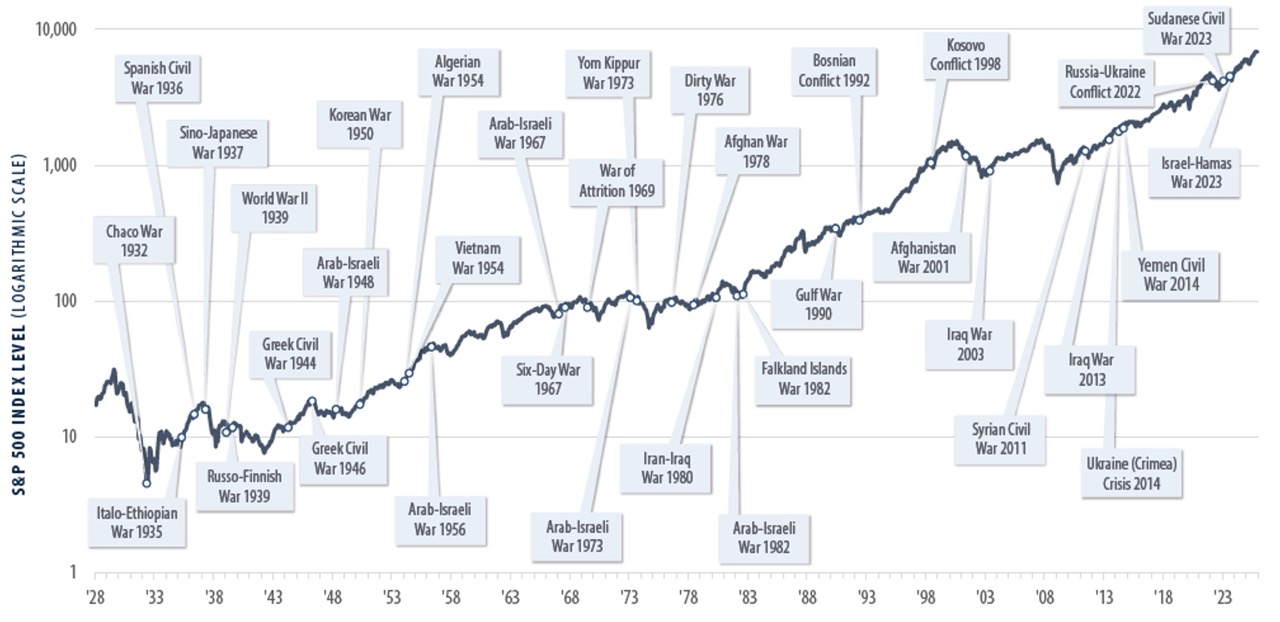

While periods of war and geopolitical conflict are understandably unsettling, history has shown that markets have consistently recovered and continued their long-term upward trajectory despite these crises.

Source: First Trust, S&P CapIQ, Bloomberg. Monthly index levels from 1928 – 2025.

As always, we appreciate your continued trust and partnership.

Manhattan West Asset Management, LLC (“MWAM”) is an SEC registered investment adviser located in California. MWAM may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. This summary should not be construed by any consumer and/or prospective client as MWAM’s rendering of personalized investment advice. Any subsequent, direct communication by MWAM with a prospective client shall be conducted by a representative that is either registered or qualifies for an exemption or exclusion from registration in the state where the prospective client resides. For information pertaining to the registration status of MWAM, please contact the United States Securities and Exchange Commission on their web site at www.adviserinfo.sec.gov. A copy of MWAM’s current written disclosure brochure discussing MWAM’s business operations, services, and fees is available upon written request.