The 30-year mortgage rate recently fell below 6%, its lowest level since September 2022, renewing interest among homebuyers and homeowners considering refinancing.

While many borrowers assume mortgage rates move directly with Federal Reserve policy and wait for signals from the Fed before locking in a rate, the relationship between the Fed Funds Rate and 30-year mortgage rates is more complex.

By understanding how mortgage rates are actually determined, buyers can identify opportunities to secure more favorable financing rather than relying on sensationalized headlines.

What is the Fed Funds Rate & Why Does it Matter?

The Fed Funds Rate is the short-term interest rate at which banks lend to one another overnight. The Federal Reserve adjusts this rate every 6 weeks to influence inflation and economic growth. While it shapes the broader interest-rate environment, it does not directly determine the interest rates on credit cards, business loans, or mortgages.

What Affects Your 30 Year Mortgage Rate?

Banks don’t use the Federal Funds Rate to determine mortgage rates. They factor in their own credit risk, funding costs, and overall profit margins when setting consumer rates, meaning a fed funds cut doesn’t automatically translate into a lower interest rate for borrowers.

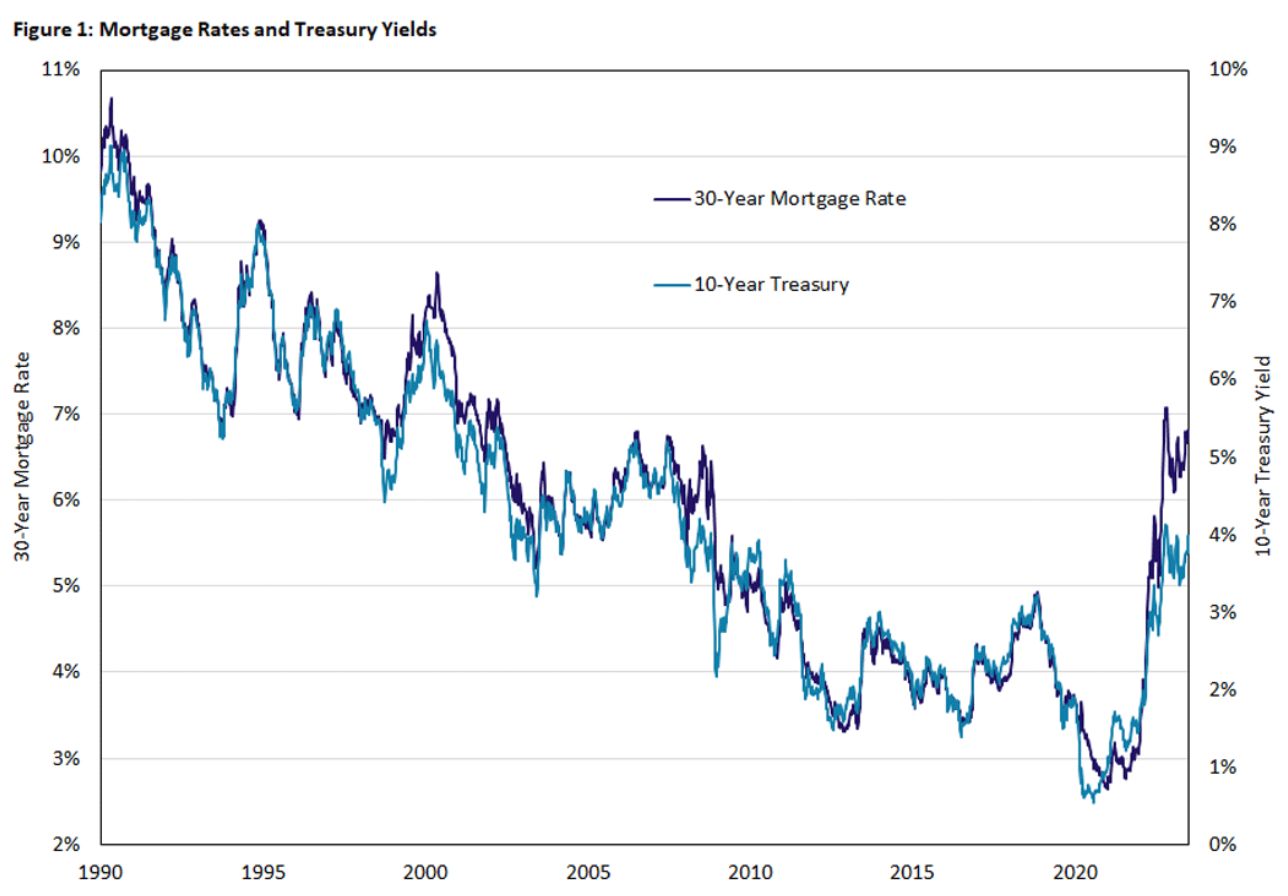

30-year mortgage rates are more closely tied to the 10-year Treasury yield, which serves as a benchmark for long-term interest rates in the U.S. financial system. Mortgage rates are typically priced relative to Treasury yields because investors compare mortgage-backed securities to government bonds when determining the returns they require.

Mortgage lenders typically price loans based on bond market yields plus a risk premium, which means mortgage rates generally move in the same direction as the 10-year Treasury, but they are not identical.

Although mortgage rates follow Treasury yields closely, they can diverge when:

- Inflation expectations change.

- Demand for mortgage-backed securities shifts.

- Housing markets become volatile.

- Banks adjust lending standards.

Source: Federal Reserve Bank of Richmond Economic Brief of August 2023

If markets believe inflation will fall or economic growth stalls, long-term Treasury yields can decline, even if the Fed Funds Rate is still holding short-term rates high. Additionally, Treasury yields can rise even before the Federal Reserve actually raises rates if investors expect tighter policy ahead.

A clear example recently occurred in September 2024. The Federal Reserve lowered the Federal Funds Rate by 0.5 percentage points, yet mortgages rose. The average 30-year mortgage rate increased from 6.09% in September to a peak of 6.84% by late November because bond markets were adjusting their inflation and growth expectations in response to strong economic data and inflation that proved more stubborn than originally forecasted.

6 Ways To Secure A Lower Interest Rate

Homebuyers have several ways to improve the mortgage rate they receive, regardless of where interest rates are in the broader market.

1. Improving Your Credit Score

Lenders price mortgages based heavily on credit quality. Borrowers with credit scores above 740 typically qualify for the lowest available mortgage rates.

2. Increase Your Down Payment

A 20% down payment reduces lender risk, lowers the loan amount, and eliminates private mortgage insurance, which can significantly reduce monthly costs.

On a $1M home at 6%, putting 20% down can save over $230,000 in interest over the life of the loan while also reducing the monthly payment by about $1,200.

3. Compare Multiple Lenders

Mortgage rates can vary significantly between lenders. Shopping for multiple quotes can reduce borrowing costs. Homebuyers should compare large commercial banks with local credit unions.

4. Consider Discount Points

Borrowers can pay upfront fees to reduce their interest rate.

5. Lock In Your Lower Rate

If rates fall below key thresholds, locking the rate protects buyers from market volatility.

6. Choose Shorter Loan Terms

15-year mortgages typically carry lower rates than 30-year mortgages.

Conclusion

The Fed Funds Rate is more than a policy lever. It reflects economic priorities and drives borrowing costs, investment behavior, and financial conditions worldwide, but does not directly set the rate on your mortgage.

Mortgage rates are influenced by many factors beyond Federal Reserve policy, including bond markets, inflation expectations, and lender risk assessments.

For homebuyers, the most important takeaway is that securing a better mortgage rate depends not only on market conditions but also on borrower decisions. Improving credit, increasing down payments, comparing lenders, and monitoring interest-rate trends can all meaningfully reduce borrowing costs over time.

Those who take the time to understand the Fed Funds Rate, 10-year Treasury Yields, and their ripple effects will be better positioned to make confident, informed, and long-term financial decisions.